Bike Rental Insurance: What Operators Actually Need

You open the email from your insurer and the renewal quote is 40% higher than last year. No claims. No changes to your fleet. Just a line about "increased sector risk." You sign it anyway because one uninsured lawsuit would cost ten times more than the premium.

Bike rental insurance is non-negotiable. But most operators either carry too little coverage or pay too much for policies loaded with exclusions that leave the biggest risks uncovered. The gap between what you think you are covered for and what the policy actually pays out is where shops go under.

This guide breaks down the four core coverage types, what they actually cost, where the gaps hide, and how waivers and multi-location policies fit into the picture. If you are still building your bike rental operation, start with our complete bike rental business guide for the full playbook.

Coverage Types Explained

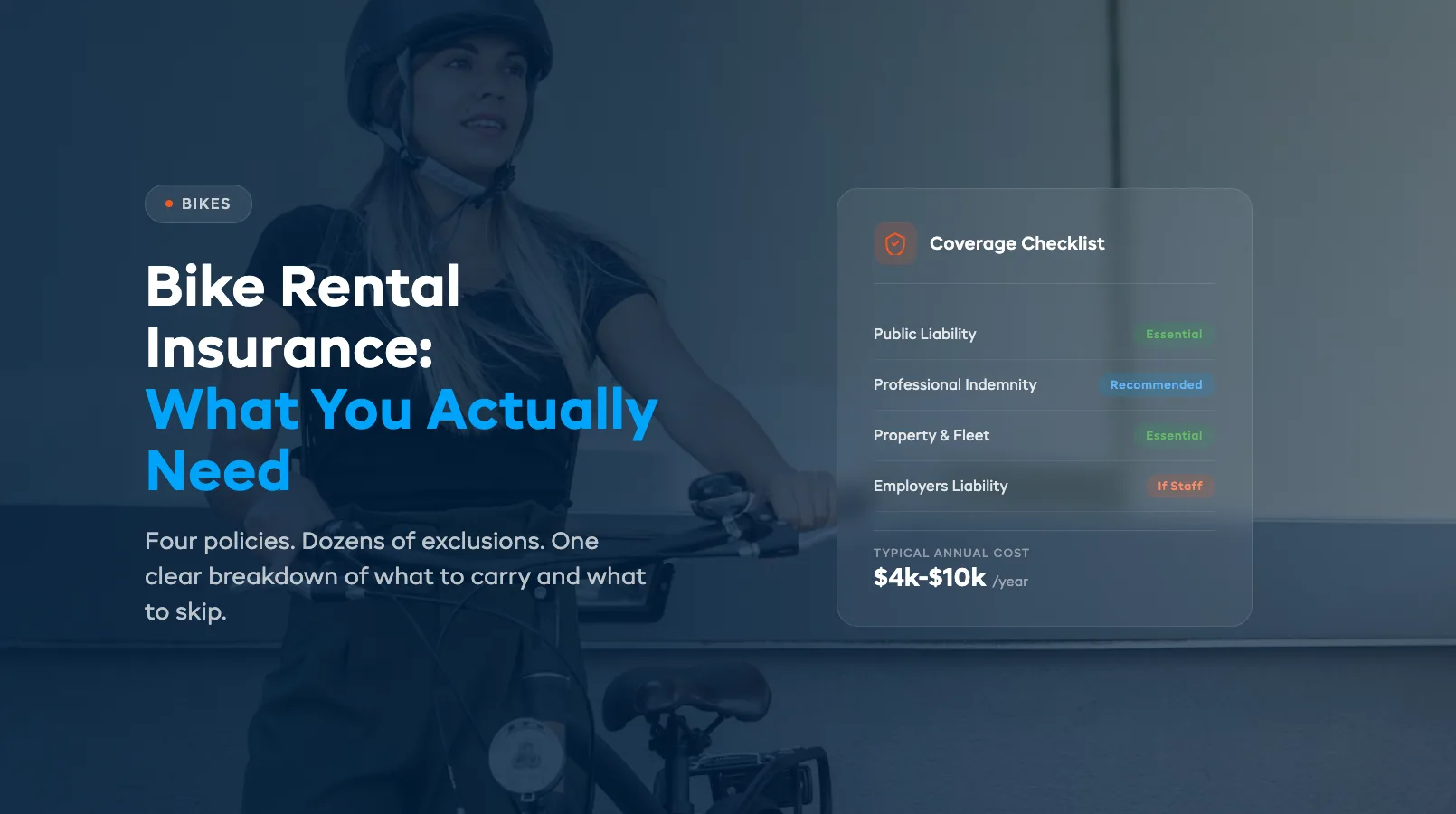

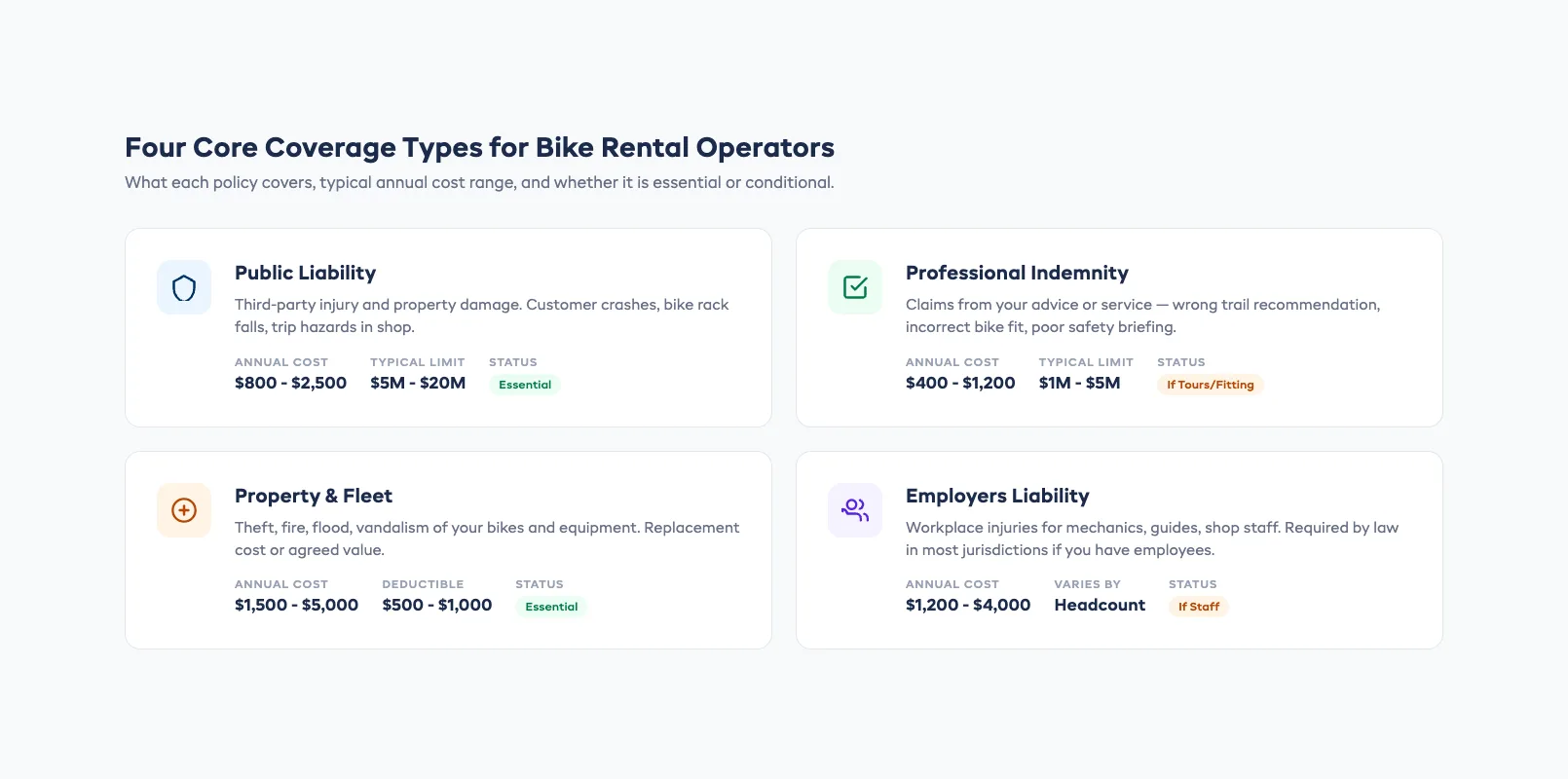

Four policies cover the core risks for bike rental operators. Most insurers bundle two or three into a single package, but understanding each one separately helps you spot what is missing.

Public liability. This is the big one. It covers injury or property damage to third parties — a customer crashes into a pedestrian, a bike rack falls on a parked car, a tourist trips over a wheel in your shop. Limits typically start at $5 million and go up to $20 million. If you only carry one policy, this is it.

Professional indemnity. Covers claims arising from your advice or service. You recommend a trail and the rider gets hurt on a section you described as "easy." You fit a helmet incorrectly. You provide a bike that is too large for the rider and they lose control. Professional indemnity kicks in where public liability stops — when the claim is about your expertise, not just an accident.

Property and fleet insurance. Covers damage to, loss of, or theft of your bikes and equipment. This is not customer-caused damage (that is what deposits and damage policies handle). This is a van full of e-bikes getting stolen overnight. A shop fire. Flood damage during off-season storage. Replacement-cost policies pay what a new equivalent bike costs. Agreed-value policies pay a pre-set amount. Replacement cost is almost always better for rental fleets.

Employers liability. Required in most jurisdictions if you have staff. Covers workplace injuries — a mechanic cuts their hand on a spoke, a guide crashes during a lead ride, a shop assistant lifts a heavy e-bike and hurts their back. Minimum limits vary by state and country. In Australia it is covered by WorkCover. In the US you need a separate workers compensation policy. In the UK employers liability is a legal requirement with a minimum of 5 million pounds.

Typical Costs

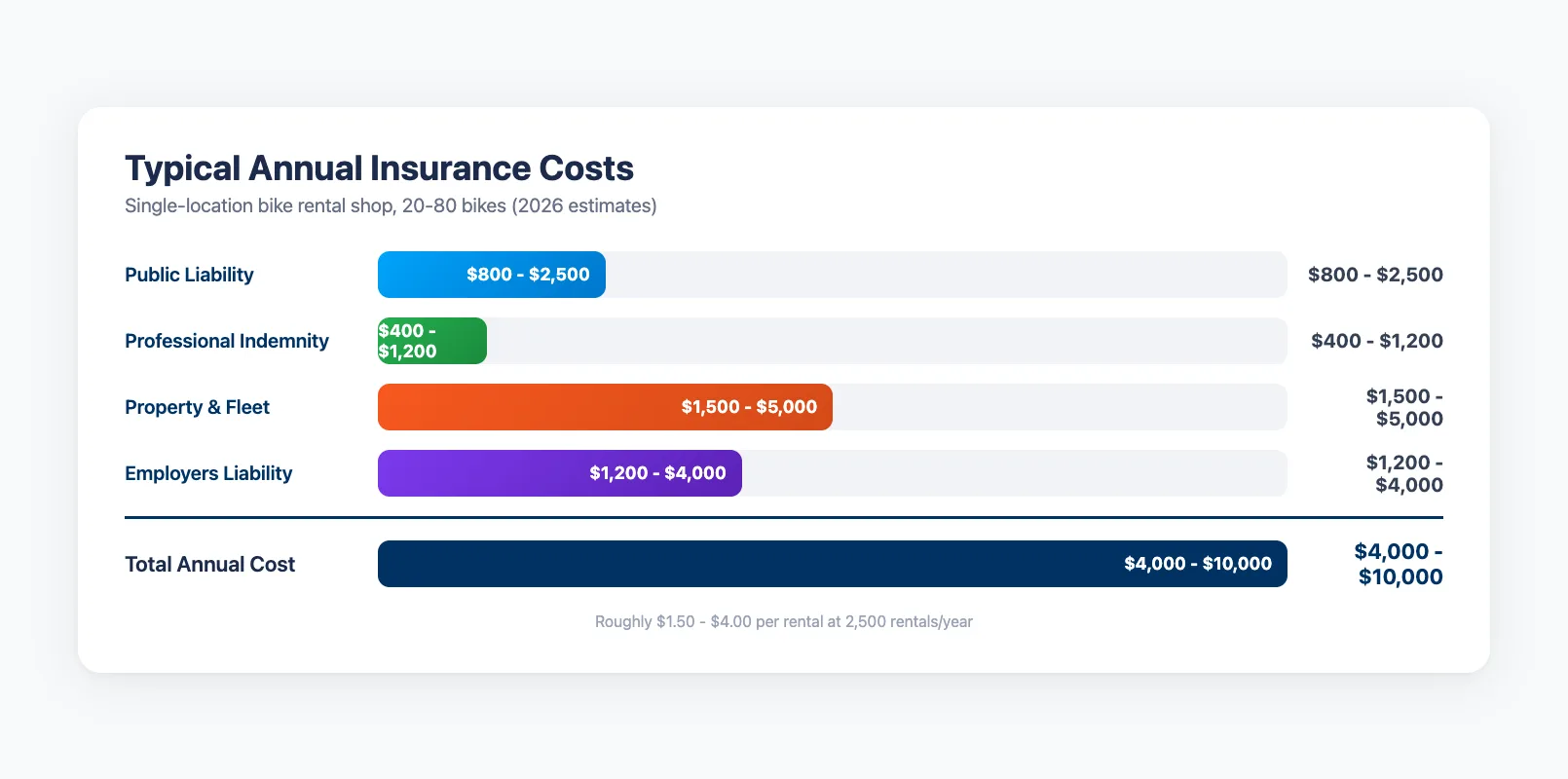

Insurance costs vary by fleet size, location, revenue, and claims history. But here are the ranges most bike rental operators see in 2026.

Public liability. $800-$2,500/year for a single-location shop with 20-80 bikes. E-bike fleets push premiums 15-30% higher because of speed-related injury risk. Tour operators who run guided rides on public roads pay more than shops offering self-guided hourly rentals.

Professional indemnity. $400-$1,200/year. Required if you run guided tours, bike fitting services, or provide trail recommendations. Some public liability policies include a professional indemnity endorsement — check before buying a separate policy.

Property and fleet insurance. $1,500-$5,000/year depending on fleet value. A 40-bike fleet of pedal bikes worth $30,000 total might cost $1,800/year. The same fleet value in e-bikes could run $3,200 because replacement parts cost more and theft rates are higher. Deductibles typically sit at $500-$1,000 per claim.

Employers liability / workers comp. $1,200-$4,000/year depending on headcount and job classifications. Mechanics and guides carry higher premiums than front-desk staff. Seasonal businesses can sometimes negotiate pro-rated premiums for peak-only coverage.

Total annual cost for a typical single-location bike rental shop: $4,000-$10,000. That works out to roughly $1.50-$4.00 per rental if you are doing 2,500 rentals per year. Build it into your pricing — most operators add a $2-$5 "insurance and safety" line item or bake it into the hourly rate.

Coverage Gaps

Every policy has exclusions. These are the ones that catch bike rental operators most often.

Customer injuries on their own bikes. If a customer rents a bike and crashes without involving a third party, public liability may not cover their medical bills. Some policies treat self-inflicted customer injuries as "assumed risk" and exclude them entirely. This is the single biggest gap in most bike rental insurance.

E-bike battery incidents. Lithium-ion battery fires during charging or storage are increasingly excluded from standard property policies. You may need a specific endorsement or a separate policy for battery storage facilities. If you run e-bikes, ask your broker explicitly about battery fire coverage. For more on e-bike operational risks, see our e-bike operations guide.

Off-premises coverage. Your fleet insurance might only cover bikes at your registered business address. Bikes stored at a hotel partner, transported in a van, or parked at a trailhead pickup point may not be covered unless you add an off-premises endorsement. This matters if you run hotel partnerships or deliver bikes to rental locations.

Wear-and-tear claims. Fleet insurance covers sudden damage, not gradual deterioration. A cracked frame from a crash is covered. A cracked frame from metal fatigue after 3,000 rentals is not. This is why maintenance schedules matter — they catch failures before they become claims.

Unaccompanied minors. If a parent rents a bike for a 14-year-old and the child gets hurt, liability coverage may be reduced or voided if your policy requires adult supervision and you did not enforce it. Check your policy language around minors and ensure your checkout process matches.

Waivers as a Complement

Insurance pays the claim. Waivers reduce the number of claims that reach your insurer in the first place. They are not interchangeable — you need both.

What waivers do. A properly drafted liability waiver gets the customer to acknowledge the risks of cycling, confirm they are physically able to ride, and agree not to sue for injuries caused by inherent risks. In most US states and Australian states, a well-drafted waiver holds up for inherent activity risks. It will not hold up for negligence — if you rent out a bike with faulty brakes, no waiver protects you.

What waivers do not do. They do not replace insurance. A waiver is a first line of defence that filters out opportunistic claims. Your insurance handles everything that gets past the waiver — genuine negligence, third-party injuries, property damage.

Digital waivers save time and create records. Paper waivers get lost, signatures get challenged, and nobody reads the fine print. Digital waivers with timestamped electronic signatures create an auditable trail your insurer will love. When a claim comes in, you can pull up the signed waiver in seconds instead of digging through a filing cabinet. Dash keeps signed waivers attached to each booking automatically, so the record is always there when you need it.

Waiver-insurance alignment. Your waiver language should mirror your policy terms. If your insurer excludes coverage for riders under 16, your waiver should not accept riders under 16. If your policy requires helmets, your waiver should include a helmet acknowledgment. Misalignment between your waiver and your policy is how claims fall through both safety nets.

Use our Pre-Rental Bike ABC Check template to make sure every bike goes out in insurable condition, and set up the Bike Damage Report Drafter to auto-generate incident documentation when a claim comes in.

Multi-Location Policies

Running bikes at two or more locations changes your insurance needs. A single blanket policy is almost always cheaper than separate policies per location, but it comes with coordination requirements.

Blanket vs per-location. A blanket policy covers all locations under one limit. If your total limit is $10 million and a claim arises at Location B, the full $10 million applies — not a fraction. Per-location policies give each site its own independent limit but cost 30-50% more in total premiums.

Schedule of locations. Your insurer needs a current list of every address where bikes are stored, rented, or serviced. Add a hotel partnership or a pop-up trailhead station and forget to notify your insurer? That location may not be covered. Update your schedule before the bikes arrive, not after.

Fleet movement between locations. If you shift bikes between shops based on demand, confirm your transit coverage. Some policies only cover bikes in transit if they are in a locked vehicle. Riding 15 bikes from Shop A to Shop B on public roads with staff? That might be uncovered unless you have specific in-transit endorsement.

Multi-state or multi-country operations. Regulatory requirements differ between jurisdictions. Workers comp in California is not the same as WorkCover in Victoria. If you operate across borders, your broker needs to build a program that satisfies every local requirement. Do not assume one policy covers everything.

Claims Process

When something goes wrong, the first 24 hours determine whether your claim gets paid quickly or gets stuck in review for months.

Step 1: Document everything immediately. Photos of the bike, the scene, any injuries. Rider's name, contact details, and waiver status. Witness statements if available. Time, date, weather conditions. The more you document at the scene, the less your insurer has to investigate later.

Step 2: Notify your insurer within 24 hours. Most policies require "prompt notification." Some define that as 24 hours, others as 48 or 72. Do not wait. Late notification is the most common reason claims get reduced or denied. Call your broker first, then follow up in writing.

Step 3: Do not admit fault. This is standard across every insurance policy in every jurisdiction. Express concern, help the injured party, call emergency services if needed — but do not say "it was our fault" or "we should have checked that brake." Let the investigation determine fault.

Step 4: Preserve the bike. Do not repair, modify, or dispose of the bike involved in an incident until your insurer gives clearance. They may want an independent inspection. Tag it, lock it in a back room, and document its condition with photos and video.

Step 5: Cooperate with the investigation. Your insurer's adjuster will request your maintenance records, rental agreements, waiver, staff training logs, and incident report. Having these organised in advance — ideally in a digital system rather than a filing cabinet — speeds settlement by weeks. Dash stores maintenance logs, signed waivers, and booking records in one place, which makes pulling claim documentation a five-minute job instead of an all-day dig.

Average settlement timeline. Simple property claims (stolen bike, vandalism) settle in 2-6 weeks. Injury claims with clear liability take 2-6 months. Disputed injury claims can take 12-18 months or longer. The better your documentation, the faster the resolution.

FAQ

Do I need insurance if I only rent 10 bikes?

Yes. Fleet size does not change your liability exposure. One customer on one bike can create a claim that exceeds your total business value. Public liability insurance is non-negotiable regardless of scale. Premiums for small fleets start around $800/year.

Does my insurance cover e-bikes differently than pedal bikes?

Usually yes. E-bikes are classified as higher risk because of motor-assisted speeds and lithium-ion battery hazards. Premiums run 15-30% higher. Battery fire and charging-related incidents may need a separate endorsement. Declare your e-bike count accurately — underreporting voids coverage.

Can a liability waiver replace insurance?

No. Waivers reduce frivolous claims by establishing assumed risk. They do not cover negligence, third-party injuries, or property damage. Insurance handles what waivers cannot. You need both working together.

What happens if a customer refuses to sign a waiver?

You have two options: refuse the rental or accept the higher risk. Most operators make waiver signing a non-negotiable condition of rental. Without a signed waiver, you lose your first line of legal defence. Your insurer may also view unsigned waivers as a failure in your risk management process.

How do I reduce my premiums?

Maintain a clean claims history. Implement documented maintenance schedules. Use digital waivers with every rental. Install security cameras and GPS trackers on high-value bikes. Train staff on safety procedures and keep training records. Every risk reduction measure you can document gives your broker leverage at renewal.

Does insurance cover bikes stored at a partner hotel?

Only if your policy includes off-premises coverage or you have added the hotel address to your schedule of locations. Bikes stored at unlisted addresses are typically excluded. Update your insurer before deploying bikes to any new site.

What is the most common reason bike rental claims get denied?

Late notification. Most policies require you to notify your insurer within 24-72 hours of an incident. Missing that window — even by a few days — gives your insurer grounds to reduce or deny the claim. Report every incident immediately, even if it seems minor at the time.

in one place