Guide Certifications: What Your Insurance Actually Requires

You've got three guides on your team. All three ran trips last weekend. One guide's Wilderness First Responder cert expired six weeks ago. Nobody noticed. If someone had been injured on that trip, your insurance company would have noticed — and your $25,000 general liability policy might have paid exactly zero.

This is the gap most adventure operators don't see until it's too late. Your insurance policy doesn't just require "certified guides." It requires specific certifications, current as of the date of the incident, matching the activity you're permitted to run. Miss any piece and you're operating without a net.

This guide maps certifications to insurance requirements so you know exactly what your team needs, what it costs, and how to track renewals before they become coverage gaps. For the full operator playbook, see How to Run an Adventure Activity Business.

The Cert-Insurance Matrix: What Connects to What

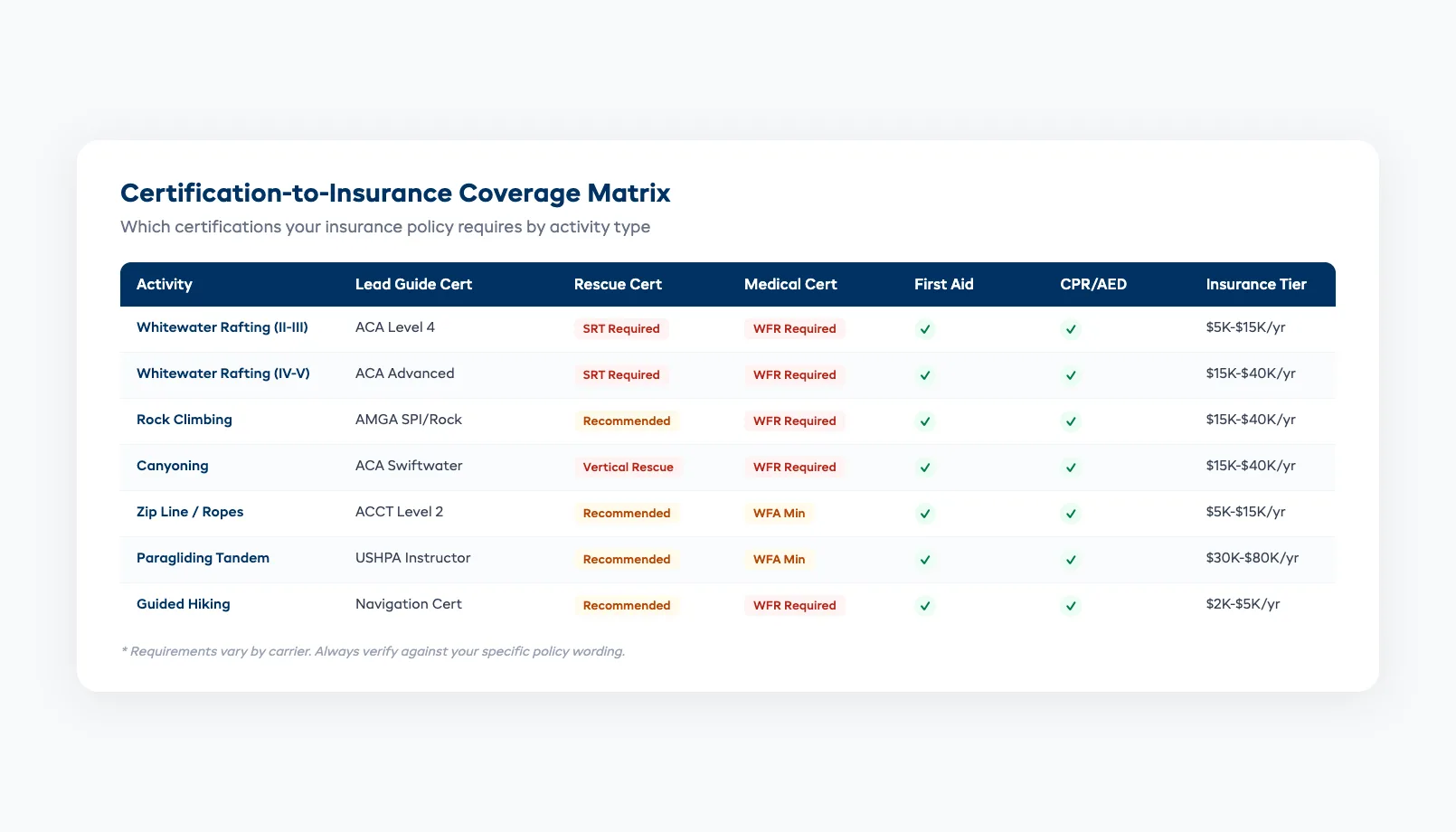

Insurance underwriters don't care about your guides' Instagram following or their years on the river. They care about documented, current credentials from recognised certifying bodies. Here's how the mapping works across common adventure activities.

Whitewater rafting. Your general liability policy almost certainly requires ACA (American Canoe Association) certification for lead guides. Most underwriters also require Swiftwater Rescue Technician (SRT) certification for at least one guide per trip. Wilderness First Responder (WFR) is required by roughly 80% of adventure insurance providers for any activity more than one hour from a hospital.

Rock climbing and canyoning. AMGA (American Mountain Guides Association) certification is the gold standard. Single Pitch Instructor for top-rope and sport climbing operations. Rock Guide certification for multi-pitch. Your insurer will specify which level matches your permitted activities. Operating a multi-pitch climbing operation with only SPI-certified guides? That's a coverage gap.

Zip line and ropes courses. ACCT (Association for Challenge Course Technology) practitioner certification is the industry baseline. Your policy likely requires Level 2 practitioner status for anyone inspecting or maintaining the course — not just operating it.

Paragliding. USHPA (United States Hang Gliding & Paragliding Association) instructor ratings are non-negotiable. Tandem Instructor rating for tandem operations. Your policy will specify the exact USHPA rating level required.

The universal requirement: first aid. Nearly every adventure insurance policy requires current first aid certification for all guides on active duty. WFR for remote activities, Wilderness First Aid (WFA) minimum for front-country operations. CPR/AED certification is assumed — if yours has lapsed, your coverage may have too.

Typical Certifications Required by Activity

Not every activity demands the same credential stack. Here's what a typical insurance policy expects for each role, broken down by activity type.

Lead guide certifications:

- Whitewater rafting (Class II-III): ACA Level 4 Whitewater Kayak Instructor or equivalent + SRT + WFR

- Whitewater rafting (Class IV-V): ACA Advanced Whitewater + SRT + WFR + minimum 200 logged trip days

- Rock climbing (outdoor): AMGA SPI or Rock Guide + WFR + current anchor-building assessment

- Canyoning: ACA Swiftwater + vertical rescue cert + WFR

- Zip line/ropes course: ACCT Level 2 Practitioner + first aid

- Guided hiking (backcountry): WFR + navigation certification (varies by jurisdiction)

- Paragliding tandem: USHPA Tandem Instructor + first aid

Assistant guide certifications (minimum):

- First aid (WFA or higher)

- CPR/AED

- Activity-specific safety training (documented in-house training acceptable for some policies, but not all)

The fine print check. Pull out your current policy. Search for "certification," "credential," and "qualification." Highlight every specific requirement. Compare that list against your actual guide roster. Most operators who do this exercise for the first time find at least one gap. If you're tracking this across a team of 5+ guides, use the Guide Certification Tracking checklist to stay ahead of renewals.

What Certifications Actually Cost

Certification isn't free, and the costs add up fast across a team. Budget for initial certification, renewals, and the time your guides spend in courses instead of running revenue trips.

Initial certification costs:

| Certification | Course Duration | Cost (USD) | Renewal Cycle |

|---|---|---|---|

| Wilderness First Responder (WFR) | 9-10 days | $800-$1,200 | Every 2-3 years |

| Swiftwater Rescue Technician (SRT) | 3-4 days | $500-$800 | Every 3 years |

| ACA Level 4 Instructor | 4-5 days + assessment | $600-$1,000 | Every 5 years |

| AMGA Single Pitch Instructor | 6-day course + exam | $1,800-$2,500 | Every 3 years |

| AMGA Rock Guide | Multi-phase, 30+ days total | $5,000-$8,000 | Every 3 years |

| ACCT Level 2 Practitioner | 3-4 days | $500-$900 | Every 3 years |

| USHPA Tandem Instructor | Varies (mentor-based) | $2,000-$4,000 | Annual |

| CPR/AED | 1 day | $50-$100 | Every 2 years |

The real cost is lost revenue. A guide spending 10 days in a WFR course during peak season costs you the course fee plus 10 days of trip revenue. For a guide running $500/day trips, that's $5,800-$6,200 total cost per WFR certification. Schedule training in the off-season wherever possible — our seasonal adventure business management guide covers how to structure off-season training budgets alongside cash flow planning and guide retention.

Team cost example. A mid-size rafting operation with 6 guides needs: 6x WFR ($6,000), 6x SRT ($3,600), 6x ACA ($4,800), 6x CPR ($360). Initial certification budget: ~$14,760 plus lost revenue from training days. Annual renewal budget: roughly $4,000-$6,000 per year to keep everyone current.

Renewal Tracking: The System That Keeps You Covered

Certifications expire. Guides forget. Seasons get busy. The operators who don't get caught with lapsed credentials are the ones who build a system — not the ones who rely on memory.

The 90-60-30 rule. Set three alerts for every certification:

- 90 days out: Notify the guide. Book the renewal course. Confirm availability.

- 60 days out: Confirm enrolment. Arrange schedule coverage for training days.

- 30 days out: Final check. If the guide hasn't enrolled, pull them from the active roster until they're re-certified.

What to track for each guide:

- Full name and employee ID

- Each certification held (issuing body, cert number, date issued, expiry date)

- Renewal course date (booked or completed)

- New cert number and updated expiry

- Copy of the physical/digital certificate on file

Centralise the tracking. Spreadsheets work until they don't — which is usually when you have 8+ guides with 3-4 certs each. That's 24-32 individual expiry dates to monitor. Dash AI can flag upcoming certification expirations automatically through the Guide Certification Expiry Alerts agent, sending notifications to both the operator and the guide 90 days before expiry.

Document everything. Keep digital copies of every certificate. When your insurer asks for proof of guide qualifications — and they will, especially after a claim — you want to produce the full record in minutes, not days.

Grandfathering: When Experience Replaces Paper

Some certifying bodies grandfather experienced practitioners when they update their standards. Others don't. This creates a grey area that can affect your insurance coverage.

How grandfathering typically works. A certifying body updates its requirements — say, AMGA adds a new assessment module to the SPI program. Guides who earned their SPI before the update may be "grandfathered" under the old standard until their next renewal cycle. At renewal, they may need to complete the new module or pass the updated assessment.

The insurance problem. Your insurer may not recognise grandfathered status. Some policies require certifications that meet "current standards as of the date of the activity." A guide operating under a grandfathered cert that no longer meets the current standard might not satisfy the policy requirement — even though the certifying body considers them certified.

How to protect yourself:

- When a certifying body updates standards, contact your insurer immediately. Ask whether grandfathered certs still satisfy policy requirements.

- Get the answer in writing. Verbal confirmations from underwriters don't hold up during claims.

- Budget for early re-certification if your insurer doesn't accept grandfathering. The re-cert cost is trivial compared to a voided claim.

- Review your policy annually during your off-season audit. Use the Pre-Season Adventure Operations Audit checklist to formalise this review.

Non-Compliance Consequences: What Actually Happens

Operators skip certifications for three reasons: cost, scheduling conflicts, and "we've been doing this for 15 years without a problem." Here's what happens when the problem arrives.

Claim denial. The most immediate consequence. Your insurer investigates a claim, discovers a guide's certification was lapsed or missing, and denies coverage. You're now personally liable for the full amount — medical bills, legal fees, settlement costs. A single serious injury claim can run $100,000-$500,000+. Without coverage, that's your money.

Policy cancellation. After a denial, your insurer may cancel your policy entirely. Getting new coverage with a cancellation on your record means higher premiums — typically 30-50% more — and fewer carriers willing to write the policy.

Permit revocation. Land management agencies (Forest Service, BLM, National Park Service) can revoke your operating permit if they discover your guides don't meet certification requirements. This has happened. Operators have lost permits they spent years obtaining because of a single uncertified guide on a single trip.

Legal liability amplification. In a lawsuit, plaintiff's attorneys look for exactly this. "The operator knew their guide's certification had expired and sent them out anyway." That's not negligence — that's recklessness. Courts treat the two very differently, and recklessness often pierces waiver protections that would otherwise shield you.

The reputational hit. In adventure tourism, word travels. Other operators talk. Land managers share notes. A single non-compliance incident can follow your business for years.

The math is simple. A WFR renewal costs $400-$600. A denied claim costs $100,000+. There is no scenario where skipping a renewal makes financial sense.

Your certifications are the bridge between running trips and being covered when something goes wrong. Build the tracking system, budget for renewals, and never send an uncertified guide into the field. The cost of compliance is a rounding error compared to the cost of a denied claim.

For the full operator playbook covering licensing, insurance, guide management, and gear lifecycle, see How to Run an Adventure Activity Business. When an incident occurs, your guide's certification status at that moment becomes critical evidence — see Adventure Incident Response and Reporting for the documentation protocol. For daily operational checklists, visit the adventure activity hub and activities glossary.

FAQ

What certifications do raft guides need for insurance coverage?

Most adventure insurance policies require ACA (American Canoe Association) certification for lead raft guides, plus Swiftwater Rescue Technician (SRT) certification for at least one guide per trip. Wilderness First Responder (WFR) is required by roughly 80% of providers for activities more than one hour from a hospital. Always check your specific policy wording — requirements vary by carrier and river classification.

How much does it cost to certify an adventure guide?

Individual certifications range from $50 (CPR/AED) to $8,000 (AMGA Rock Guide). A typical rafting guide needs WFR ($800-$1,200), SRT ($500-$800), ACA Level 4 ($600-$1,000), and CPR ($50-$100) — roughly $2,000-$3,100 in course fees plus lost revenue from training days. Budget $4,000-$6,000 per year in renewal costs for a team of 6 guides.

What happens if a guide's certification expires and there's an incident?

Your insurer will likely deny the claim. A lapsed certification means your guide didn't meet policy requirements at the time of the incident. You become personally liable for medical bills, legal fees, and settlement costs — potentially $100,000-$500,000+. Your policy may also be cancelled, making future coverage significantly more expensive.

Do insurance companies accept grandfathered certifications?

Not always. When a certifying body updates its standards, some insurers require guides to meet the new standard regardless of grandfathered status. Contact your insurer in writing whenever a certifying body updates requirements. Get explicit confirmation that grandfathered certs still satisfy your policy. Don't assume — ask.

How far in advance should I track certification renewals?

Use a 90-60-30 day system. At 90 days, notify the guide and book the renewal course. At 60 days, confirm enrolment and arrange schedule coverage. At 30 days, if the guide hasn't enrolled, remove them from the active roster until re-certified. Automated alerts through your operations platform prevent gaps from slipping through.

Can in-house training replace formal certifications for insurance purposes?

For lead guide positions, almost never. Insurance policies specify certifications from recognised bodies (ACA, AMGA, ACCT, USHPA). In-house training may satisfy requirements for assistant guides in some policies, but only when documented with dates, curriculum, instructor qualifications, and assessment results. Check your policy's exact language before relying on in-house training alone.

in one place