Insurance, Waivers, and Legal Foundations for Tour Businesses

Insurance and waivers are the part of running a tour business nobody gets into the trade for. They sit in a drawer, cost you money every year, and feel like pure overhead — until the morning a guest twists an ankle on a trail, a client's camera goes into the river, or a letter arrives from someone's lawyer. On that morning, the paperwork you set up months ago is the only thing standing between a bad day and a closed business.

The good news is that getting this right isn't complicated, and it isn't only for big operators. A solo guide running walking tours needs the same foundations as a 30-staff adventure company — just at a smaller scale. This guide walks through the coverage types that matter, what they typically cost, how to build a waiver that actually protects you, the extra protection high-risk activities demand, what the claims process really looks like, and how coverage works when you run trips across borders. It's a plain-English starting point, not legal advice — confirm the specifics with a broker and a lawyer in your region. For the wider operating picture, see How to Run a Tour Operator Business.

The Coverage Types Every Tour Operator Needs

Most operators think "insurance" means one policy. It's really a stack of separate covers, each handling a different way things can go wrong. You don't need all of them on day one, but you should know what each one is for.

- General liability is the foundation. It covers third-party injury and property damage — a guest trips on your equipment, or your group damages a venue. If you buy nothing else, buy this.

- Professional liability (sometimes called errors and omissions) covers claims that your advice or service caused harm — you led a group into conditions you should have avoided, or a booking error stranded someone.

- Participant or activity accident cover handles injuries to the people actually on your tour, which general liability often excludes for the activity itself.

- Commercial property and equipment covers your gear, vehicles, and premises against theft, damage, and loss.

- Workers' compensation is usually legally required the moment you have staff or guides on payroll, and covers their on-the-job injuries.

The mix you need depends on what you run and where. A city food-tour operator and a backcountry rafting company face very different risks, and their policies should look different too. The licensing and insurance decisions sit at the centre of setting up the business properly — a topic the operator's guide covers alongside the rest.

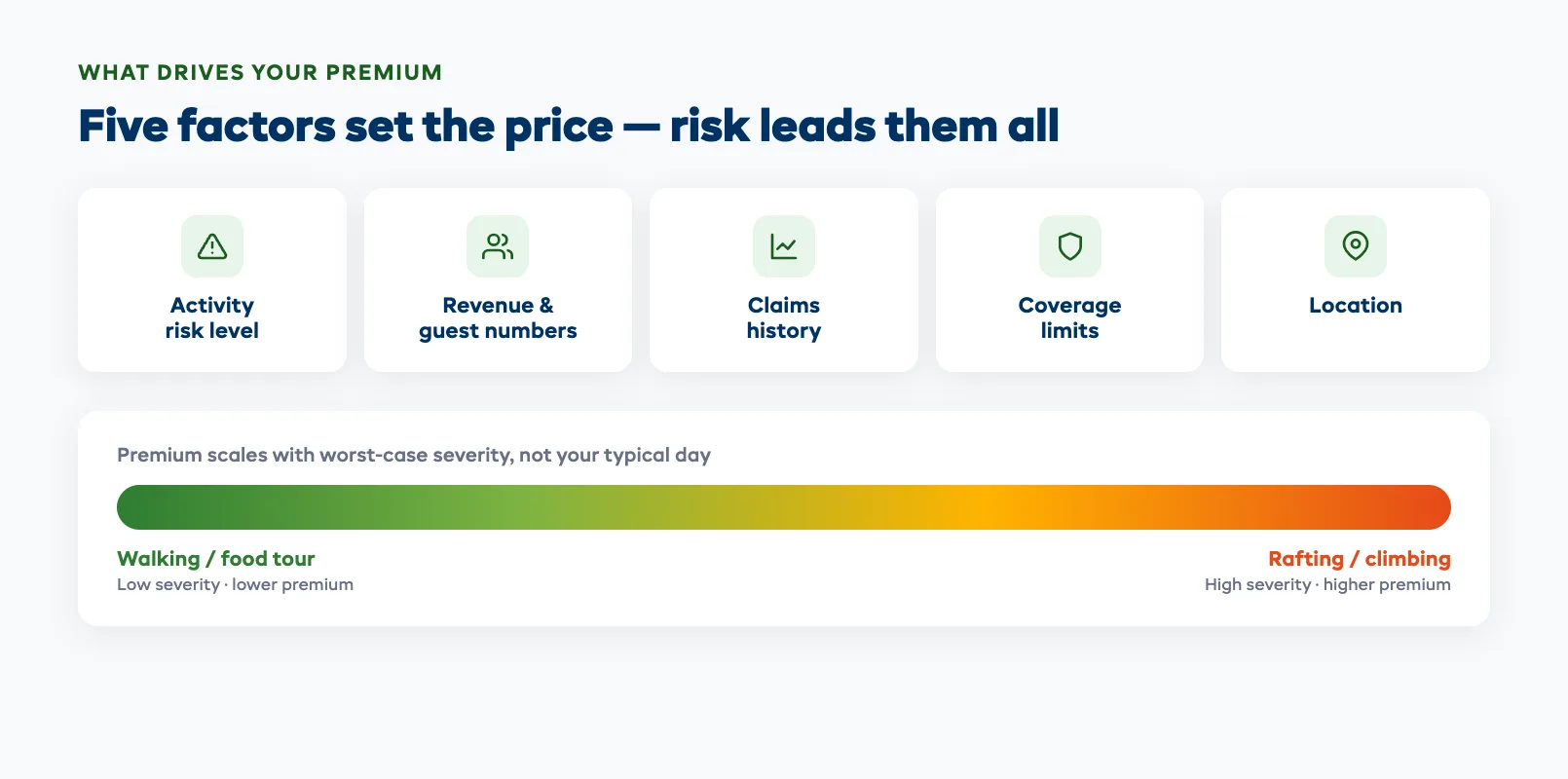

What It Typically Costs

Premiums vary so widely that any single number is misleading — but operators always want a ballpark, so here's how to think about it rather than a figure to quote.

Your premium is driven by a handful of factors: the risk level of your activities, your annual revenue and guest numbers, your claims history, your coverage limits, and your location. A guided museum walk is cheap to insure. A via ferrata or whitewater operation is not, because the worst-case injury is far more severe. A new operator with no claims history may pay more until they build a track record; an established business with a clean record earns better rates.

The practical mistake isn't paying too much — it's under-insuring to save money. Operators pick a low coverage limit to shave the premium, then discover after a serious claim that their limit doesn't come close to covering the legal costs and settlement. The fix is to match your coverage limit to your worst realistic scenario, not your typical day. Talk to a broker who specialises in tours and adventure activities; a generalist will either overcharge you or miss a gap. And revisit the policy every year, because as your guest numbers and activities grow, last season's cover quietly stops being enough.

Waivers: Your First Line of Defence

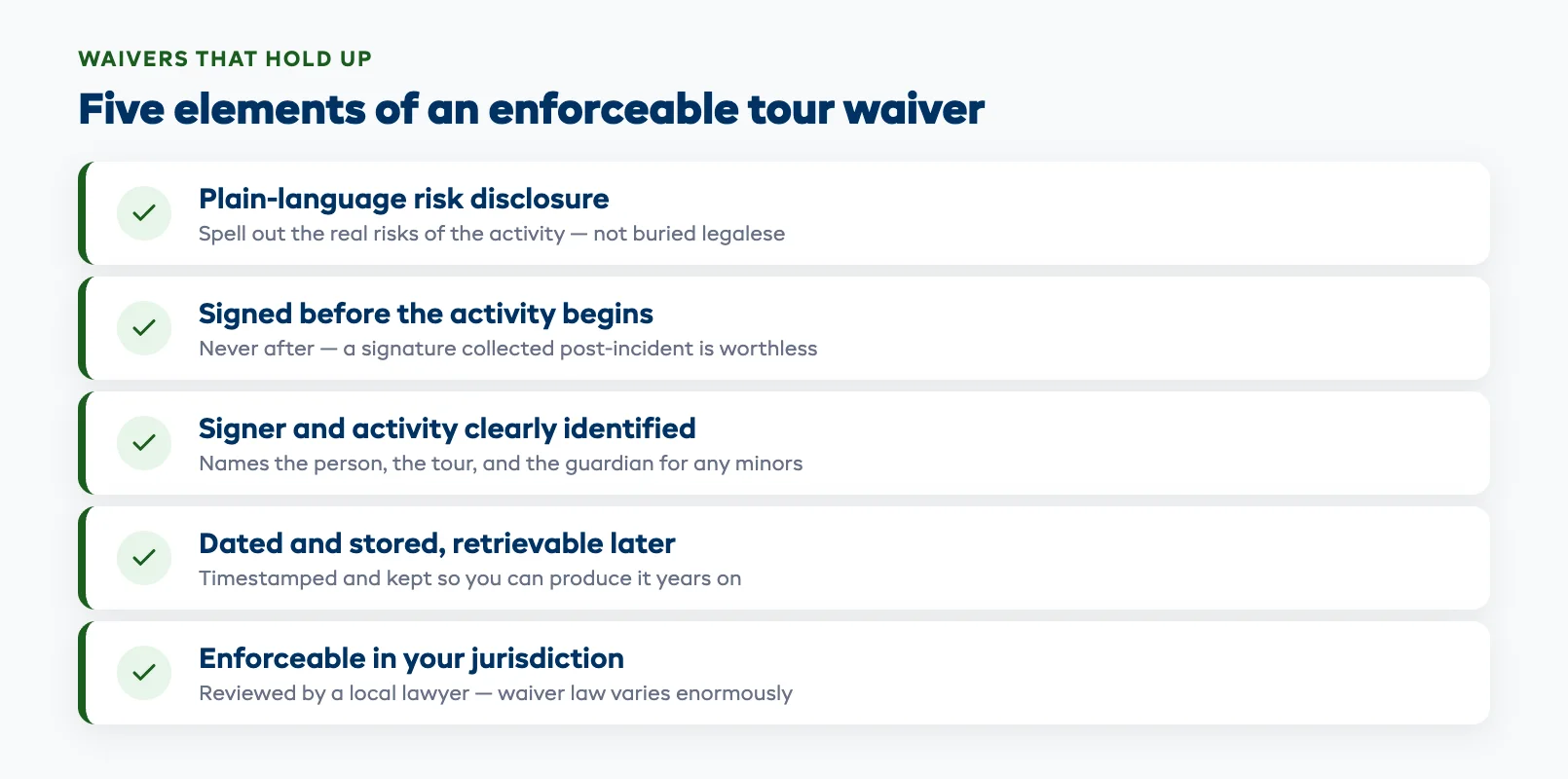

A waiver doesn't make you immune from being sued — nothing does. What a well-built waiver does is document that the guest understood the risks and agreed to them, which is often the difference between a claim that goes nowhere and one that costs you everything. Treat it as a core operating document, not a formality to rush at the trailhead.

A waiver that actually holds up shares a few traits. It spells out the specific risks of the activity in plain language rather than burying them in legalese. It's signed before the activity begins, never after. It clearly identifies the signer and the activity, and it's dated and stored so you can produce it later. Crucially, it has to be enforceable in your jurisdiction — waiver law varies enormously, and a clause that protects you in one place is worthless in another, which is exactly why a local lawyer should review your template.

The operational side matters as much as the wording. A perfect waiver no one signed is worthless, and chasing signatures on a busy departure morning is how guests slip through unsigned. The reliable fix is to collect waivers digitally, attached to the booking, before the guest arrives — so your check-in screen shows who's cleared and who isn't. A waiver-chaser agent can nudge the unsigned automatically in the days before a trip, and keeping waivers inside your booking system rather than a separate app is the single biggest reliability upgrade most operators can make. That case is laid out in full in tour operator software with built-in waivers.

Activity-Specific Additions for High-Risk Tours

The higher the risk, the more your insurer cares about the details — and the more they'll exclude if you don't disclose properly. Adventure activities like climbing, diving, rafting, ziplining, and motorised tours almost always need named cover for each specific activity, not a generic policy that "should" apply.

Three things matter here. First, disclose every activity you run, honestly. If a claim arises from an activity you didn't declare, your insurer can deny it outright — and an undisclosed activity is one of the most common reasons a claim gets refused. Second, expect guide-certification requirements. Insurers for high-risk activities frequently require that guides hold current, named certifications, and they'll ask for proof at claim time. Keeping those certifications current and on file is part of the job; a guide-certification review checklist keeps it from slipping. Third, layer your waivers and briefings to match the risk — a high-risk activity deserves a specific risk disclosure and a documented safety briefing, not the same one-line waiver you'd use for a walking tour.

The mindset shift is simple: for high-risk tours, your insurance, your waivers, and your guide credentials all have to tell the same consistent story. When they don't line up, that's the gap a claim falls through.

What the Claims Process Actually Looks Like

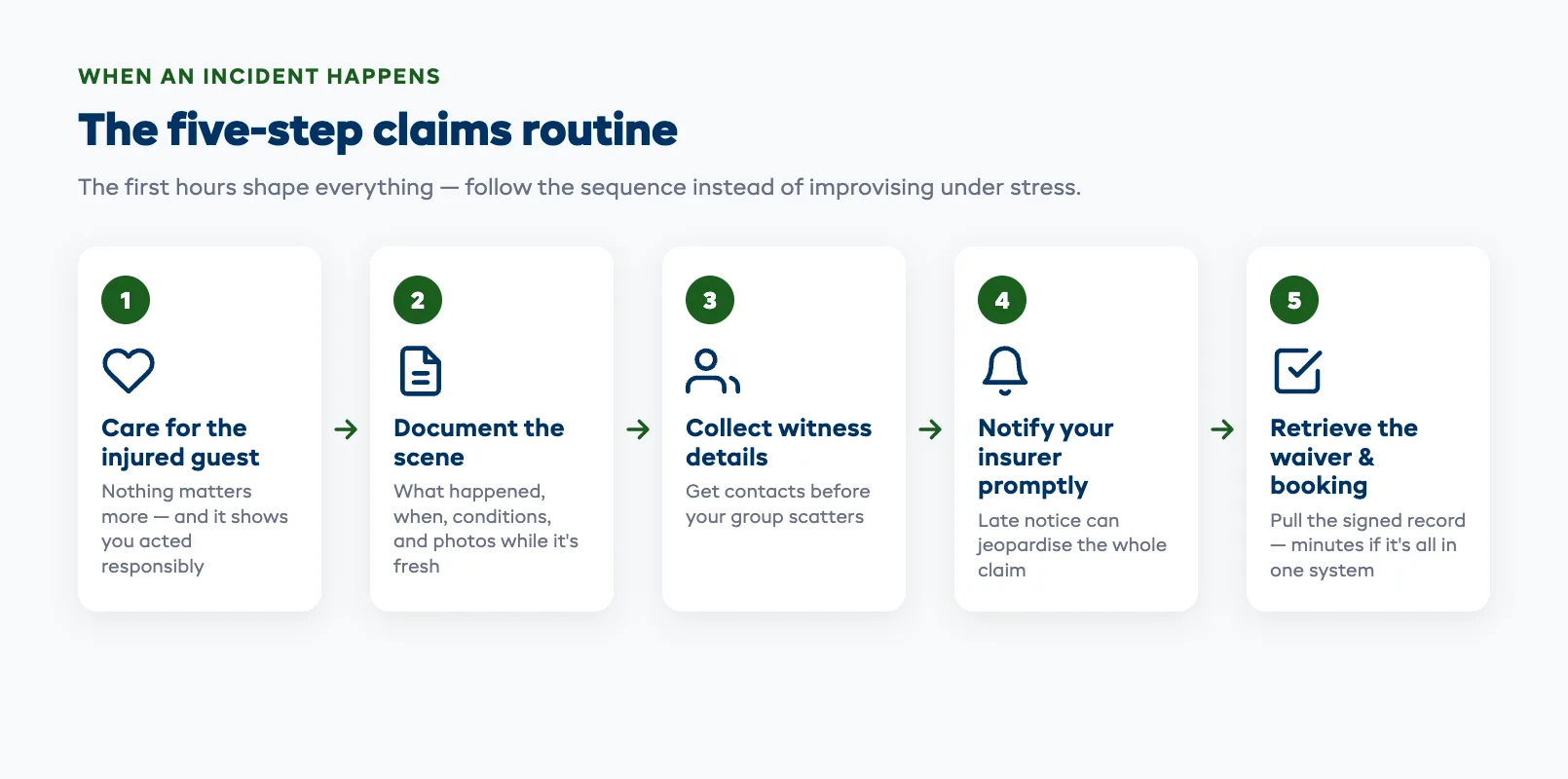

When an incident happens, what you do in the first hours shapes everything that follows. Operators who handle this well have a routine; operators who don't improvise under stress and make it worse.

The sequence is consistent. Care for the injured person first — nothing matters more, and your response is also evidence that you acted responsibly. Then document everything while it's fresh: what happened, when, who was present, conditions, and photos if appropriate. Collect witness contact details before your group scatters. Notify your insurer promptly — most policies require timely notice, and a late report can jeopardise the claim. Don't admit fault or speculate about cause in writing or to the guest; state facts, express genuine care, and let the process work. Then retrieve the signed waiver and your booking record for that guest.

This is where having a documented incident response protocol earns its keep — so any guide, on any day, follows the same steps instead of guessing. It's also where good record-keeping pays off: when your waivers, bookings, and guest details all live in one system, producing a complete, timestamped record for your insurer takes minutes instead of a frantic afternoon. The same discipline that keeps day-to-day operations calm — like a clear cancellation and no-show policy — is what makes the rare bad day manageable.

Multi-Country and Cross-Border Coverage

If you run trips in more than one country — or sell to travellers who book from abroad — coverage gets more complicated, and assumptions get expensive. A policy written for one country often won't respond to an incident in another, and you may not find out until a claim is denied.

Two questions decide what you need. Where does the activity physically take place, and where are your guests coming from? A domestic operator serving international tourists usually needs cover that responds wherever the guest later pursues a claim, which can be their home country, not yours. An operator running trips in several countries typically needs either policies in each jurisdiction or a single policy with explicit multi-territory cover — and "explicit" is the key word, because silence in a policy usually means no cover. Waiver enforceability is the same trap: a waiver valid at home may not hold where the activity happened or where the guest lives.

The rule of thumb is to never assume your coverage or your waivers travel with you. Before you run a trip in a new country or take your first overseas booking, confirm in writing with your broker that you're covered there. For the broader set of decisions around running and growing the operation, the tours hub and the tour operator glossary are good next stops.

Getting insurance and waivers right won't win you a single booking. But it's the foundation everything else stands on — and the operators who treat it as core infrastructure, not annual paperwork, are the ones still in business after the bad day that eventually comes for everyone.

FAQ

What insurance does a tour operator actually need?

Most tour operators need a stack of covers rather than one policy. General liability is the foundation, covering third-party injury and property damage. On top of that, professional liability covers claims that your advice or service caused harm, participant accident cover handles injuries to people on your tour, commercial property cover protects your gear and premises, and workers' compensation is usually legally required once you have staff. The exact mix depends on your activities and location, so work with a broker who specialises in tours and adventure to match cover to your real risks.

How much does tour operator insurance cost?

There's no single figure, because premiums are driven by your activity risk level, annual revenue and guest numbers, claims history, coverage limits, and location. A guided walking tour is cheap to insure; a rafting or climbing operation is far more expensive because the worst-case injury is more severe. The bigger risk isn't overpaying — it's under-insuring to save money and discovering your coverage limit can't cover a serious claim. Match your limit to your worst realistic scenario rather than a typical day, and review the policy every year as your business grows.

Does a waiver actually protect a tour business legally?

A waiver doesn't make you immune from being sued, but a well-built one documents that the guest understood and accepted the risks, which is often the difference between a claim that fails and one that succeeds. To hold up, a waiver should disclose the specific risks in plain language, be signed before the activity begins, clearly identify the signer and activity, be dated and stored so you can produce it later, and — most importantly — be enforceable in your jurisdiction. Because waiver law varies widely by location, have a local lawyer review your template.

What extra insurance do high-risk tour activities need?

High-risk activities like climbing, diving, rafting, ziplining, and motorised tours almost always need cover that names each specific activity, rather than a generic policy you assume applies. Disclose every activity you run honestly, because an undisclosed activity is one of the most common reasons a claim is denied. Insurers also frequently require guides to hold current, named certifications and will ask for proof at claim time, so keep those credentials current and on file. Your insurance, waivers, and guide certifications all need to tell the same consistent story.

What should I do when a guest is injured on a tour?

Follow a consistent routine instead of improvising. Care for the injured person first, both because it matters most and because your response is evidence you acted responsibly. Document what happened while it's fresh, collect witness contact details before your group scatters, and notify your insurer promptly, since late notice can jeopardise a claim. Don't admit fault or speculate about cause — state facts and express genuine care. Then retrieve the signed waiver and booking record for that guest. A documented incident response protocol ensures any guide follows the same steps under stress.

Does my tour insurance cover trips in other countries?

Not automatically. A policy written for one country often won't respond to an incident in another, and you may only find out when a claim is denied. What you need depends on where the activity physically takes place and where your guests come from. A domestic operator serving international tourists may need cover that responds wherever the guest later pursues a claim, while an operator running trips in several countries typically needs policies in each jurisdiction or a single policy with explicit multi-territory cover. Confirm in writing with your broker before running a trip in a new country or taking your first overseas booking.

in one place